In this post, I will look over the divergence in intrinsic and book value. This piece takes heavy inspiration from Warren Buffett’s 1994 Berkshire Hathaway Shareholder Letter.

The book value of a business is a number that is very easy to compute but it does have its limitations in use cases (best for banks & insurance). Unlike intrinsic value where it is impossible to calculate exactly and can be used for all businesses regardless of size or industry.

To clarify, I would define book value as the carrying value of the entire enterprise (share capital & retained earnings), which is the difference in total assets and total liabilities, its net worth. I would define intrinsic value as the discounted value of the cash distributable to owners throughout the course of the firm’s life.

The book and intrinsic values of a business can be very different. When a firm’s assets are due to produce little to no cash for owners in the future and the carrying value is more than liquidation value, the book value for the business will exceed the intrinsic value. On the other hand, when the carrying value of a firm’s assets are less than the cash benefits to owners in the future, the intrinsic value of the business exceeds the business’s book value.

In his letter to shareholders, Buffett uses the example of education (a form of investment) to explain the divergence of book & intrinsic value.

To get a figure for the intrinsic value of education, we would need to estimate the future earnings stream that a graduate would receive throughout the course of their lifetime and subtract that number by what they would’ve earned in their lifetime without a degree. The difference, discounted at the appropriate interest rate back to the day of graduation is the intrinsic economic value of education.

The cost of education should be thought of as the book value.

To evaluate whether or not the cost of education is worth it, prospectives should compare their book value to the intrinsic value of education. If the intrinsic value of education falls short of the book value, the student would not be getting their money’s worth and is better off getting a job than going to college. Some prospectives will find that their intrinsic value of education exceeds their book value, these people are far better off paying for their education and then getting employed. It is important to note that this calculation ignores the non-economic value of education that is a key factor in the decision making process for many.

In a more practical example, Buffett uses the example of Scott Fetzer (1986-1994), a Berkshire subsidiary. Acquired in 86′ Berkshire paid $315 million, a $142.6 million premium to book value. Back in the 90s, goodwill would be amortized (was changed in 01′ w/ some exceptions made in 14′), and was in the case of Scott Fetzer & Berkshire. In this example, Scott Fetzer’s carrying value on Berkshire’s books had shrunk down to $90.7 million but earnings had just short of doubled ($40.3M > $79.3M). Whilst the book value of Scott Fetzer was shrinking, the intrinsic value of the business was growing. The amortization costs of Scott Fetzer reduced Berkshire’s net worth & earnings but in truth, the intrinsic value growth strengthened the Berkshire enterprise.

In some cases, book value is a fair and useful indicator of business performance but it cannot be made out to be a substitute for intrinsic value. The calculation of intrinsic value is completely different to that of book value and far less precise. Book value is faithful to historical value, while intrinsic value fixates on future output. When evaluating possible investment opportunities, it is almost always appropriate to disregard book value for intrinsic value.

High price to earnings ratios tend to be associated with expensive share prices. But is this true? When looking at a P/E ratio in isolation high multiples don’t seem all that appealing and may result in subpar investment returns. When comparing a large and diversified list of stocks, low P/E names tend to outperform higher P/E stocks on average. But on an individual level, the fundamental makeup of companies is what should truly decide a firm’s per-share price relative to its current earning power. The price to earnings ratio doesn’t have much to do with valuation other than providing a hint as to when cash may flow into the business.

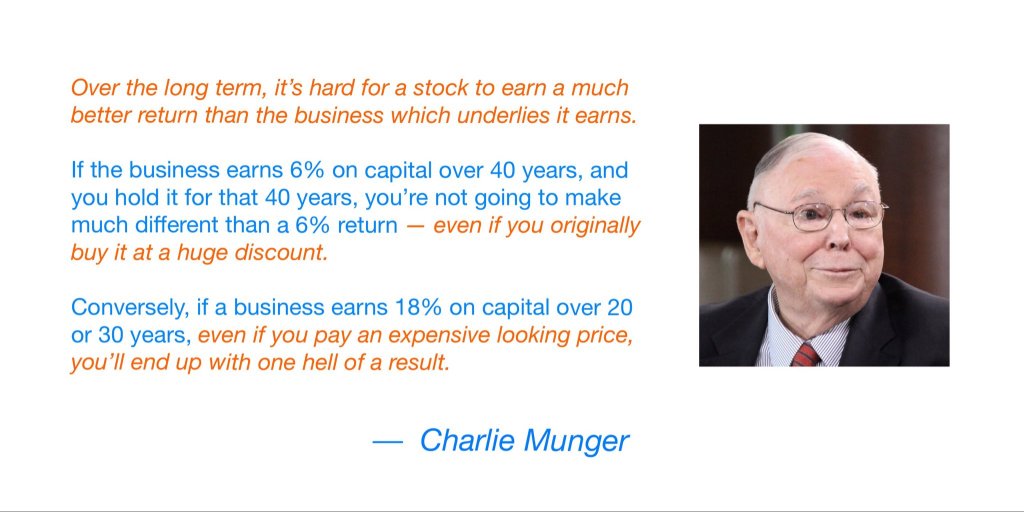

The value of a company rests on the discounted value of future cash flows generated by the business. This figure is completely independent to TTM earnings numbers and the price to earnings ratio of a stock. A more appropriate metric to look for in a business is the return on invested capital. The importance of maintaining a high ROIC is best summed up by Charlie Munger when he said:

In the short term, the per-share price of a stock can fluctuate erratically but as an investor continues to hold their shares over the long term it will match the internal returns of the business. As for the business, the best way to increase the per share intrinsic value of the firm is to retain a substantial percent of their earnings and reinvest those earnings at a high rate of return (if possible). The very few businesses that can guarantee high returns on incremental capital over an extended period will undoubtedly outperform the market. These types of businesses require durable competitive advantages to achieve such results. There are only a handful of businesses that fit this profile – many will promise these returns but are unlikely to realize them.

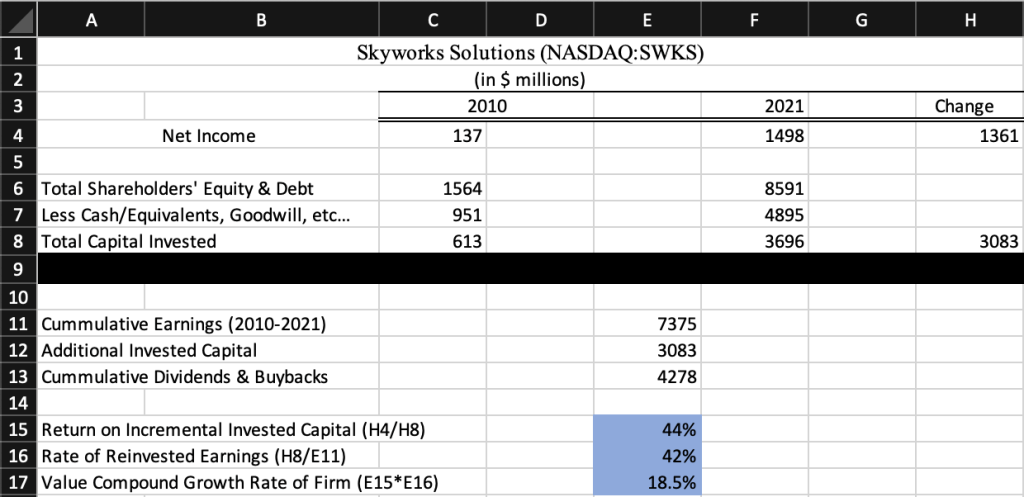

An example of one of these businesses is Skyworks Solutions. Let’s see how an investment in the business would’ve fared from 2011-2021.

In 2010, Skyworks Solutions earned $137 million in after-tax profits on $613 million of capital (minus cash, cash equivalents, goodwill, and intangibles), a return of 22%.

Fast forward to 2021, Skyworks then earned $1.49 billion in after-tax profits on $3.7 billion of capital, a return of 40.5%.

Over the 10 years, profits have increased by $1.36 billion while the company has invested an additional $3.1 billion of capital. Therefore, Skyworks’ return on additional capital employed over the 10-year period is a whopping 44%. Over the period, you can estimate that Skyworks reinvested about 42% of its earnings. By dividing the $3.1 billion of additional capital with the cumulative earnings of the period you get an estimate of the percentage of earnings reinvested into the business. Meaning for every $100 of earnings generated by Skyworks, $42 was reinvested in the business and $58 was distributed back to shareholders as dividends and/or share repurchases.

The value of the business should also over time compound at the rate at which the product of the percent of earnings reinvested and the firm’s return on invested capital equals. For Skyworks that would be a per-share compounded growth rate of 18.5% (.44*.42) and higher due to buybacks and dividends.

Skyworks Solutions stock closed on the 31st of December 2010 at a price of $28.63. 10 years later, on the same day, the stock closed at $152.88, a CAGR of 18.24% (excluding dividends), not too far off the estimated per-share growth rate using the return on incremental invested capital. Unless there is a substantial expansion in multiples, businesses with low returns on capital will see their shares match their rate and provide unsatisfactory results for shareholders.

The best kind of businesses can reinvest a substantial amount of their earnings at high rates of return for long periods of time until large numbers eventually drag down results (like the DJ Khaled album, Suffering from Success). Another great business is one that provides high rates of return but only on a small portion of reinvested earnings (a Coca-Cola or See’s Candies for example). These businesses should end up sending shareholders/owners most of their earnings or risk destroying shareholder value as the capital can no longer be deployed intelligently. By sending excess earnings to shareholders, the owners can reinvest that capital in other enterprises with more enticing opportunities. The worst businesses on the other hand require large amounts of capital to get a return that is just satisfactory (airlines). To quote Richard Branson, “the fastest way to become a millionaire in the airline business is to start out as a billionaire”.

Many other alterations can be made to find the ‘right’ numbers to calculate a firm’s return on capital. But the 2 types of businesses where owners are treated to exceptional results are very rare to find. This key metric in my opinion is more likely to tell you about the value of a business as opposed to a firm’s price to earnings ratio. The value of a business relies on future assumptions of cash flows not past earnings.

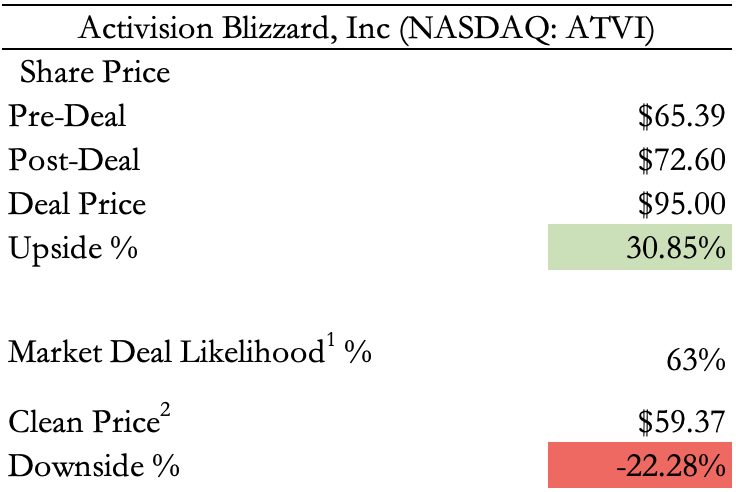

On January 18, 2022, Microsoft (NASDAQ: MSFT) announced their plans to acquire Activision Blizzard (NASDAQ: ATVI) for $95.00 per share, an all cash deal valued at $68.7 billion, inclusive of Activision Blizzard’s net cash. Should the deal close Microsoft Gaming would become the 3rd largest video game provider by revenue (behind Tencent & Sony). Microsoft hopes to close this deal by June 30, 2023, its fiscal year end. This acquisition serves as a chance for Microsoft to continue growing its gaming business on PCs, mobile phones, and consoles. However, Activision shares currently sit at $72.60 per share, representing a 30.85% upside should the deal close. Interested in this opportunity, I’ve decided to write here some of what is known of the deal and will attempt to judge the probability of the deal closing.

The Target

Activision Blizzard is one of the world’s largest video gaming publishing companies. The company owns some of the world’s most well known franchises in gaming. The Blizzard Studio houses: “Call of Duty”, “Overwatch”, “World of Warcraft”, “Diablo”, and many more. Additionally, the King Studio has “Candy Crush” and more mobile games to its name. Prior to the announcement of the deal at the turn of the year, shares saw an intra-year drawdown of over 40% in 2021 from a peak at $103 per-share. This drop was largely due to lawsuits filed against the company alleging sexual misconduct committed by executives. Over the years, Activision has been berated for its handling of sexual harassment allegations and its lack of change to remedy the problems within its workplace.

Come January, Activision shareholders quickly saw a turn in their fortunes when Microsoft announced its planned acquisition of the company for $95.00 per-share. But as I introduced earlier, shares have not climbed to that level representing the risk, mostly legal, of the deal failing to go through. I will now go over what UK & EU regulators are saying about the deal.

Legal Worries

According to Reuters, the European Commission’s biggest worry with this deal is whether Microsoft would be incentivized to block competitors off from Activision’s array of games and if that should occur, if there would be enough suppliers in the market afterwards. The EU regulators have already probed competition to find out if the acquisition would give Microsoft a competitive advantage in publishing & distribution of games across all platforms, from the user data they would receive. Game developers & publishers are also being considered as to how a deal would affect their bargaining power to sell games on Xbox and through the Game Pass (Microsoft’s Cloud Gaming subscription service). Other regulatory worries surround the “Call of Duty” franchise and potential effects of adding Activision to Windows OS.

The UK’s Competition and Market’s Authority (CMA) have continued their in-depth probe into the acquisition also being weary of the what could occur should Microsoft block rivals from Activision’s library. An area of great concern for the CMA is in the nascent cloud gaming industry, where the addition of Activision could damage competition for services.

It seems most authorities are only considering their local industry dynamics, which may prove to be a headache for Microsoft to get the deal over the line, as Tencent and other competitors may have less of a hold on certain markets.

Note: I have excluded the FTC from this discussion, as they tend to be rather toothless when it comes to stopping these deals. However, that could always change…

The Response

It seems to me that the most common concern behind the scrutiny of the transaction is the fear of Microsoft turning Activision’s library into Xbox exclusives entirely. But will this fear prove to stop the deal or is there evidence that the regulators will turn a blind eye to this. We already have precedent of Microsoft acquiring game publishers and continuing to make the games available on all platforms (also making a few exclusive, in fairness). On March 9, 2021, Microsoft finalized the acquisition of Bethesda Softworks (developer of Fallout & Doom) for $7 billion. Fast forward, a year from the finalization of the deal, Bethesda plans to release Fallout 4 in 2023 across all platforms, including close competition at Sony. Besides the size of this transaction what real change is there between the purchase of Activision and that of Bethesda? Here are a few words from the EU Commission after approving the Bethesda acquisition:

“The Commission concluded that the proposed acquisition would raise no competition concerns, given the combined entity’s limited market position upstream and the presence of strong downstream competitors in the distribution of video games”Source

I do not see any reason why regulators should fear this acquisition based on their prior approval of a similar transaction. The only difference discernible to me is the size of the deal, but when compared to the big two (in gaming revenues): Tencent & Sony, Microsoft + Activision only closes the gap in revenues and would still be around $2 billion short of Sony in 2nd place. Additionally, it is important to note that gaming has been a long continued trend of supporting cross-platform function. I do not see why Microsoft would fight against this trend, when previous acquisitions show it hasn’t done so and risk alienating potential audiences from the games they would develop themselves. Candy Crush, Call of Duty, and World of Warcraft made up 82% of Blizzard’s revenue for the fiscal year 2021, it is hard to imagine why Microsoft would make these games exclusive to its platform given the growth in cross-platform gaming. To me, it would be a misstep by Microsoft to turn the Activision library into Xbox exclusives and it would not make sense for them to do so given the rising popularity of cross-platform gaming.

The deal has already passed through regulators in Brazil & Saudi Arabia. What I found to be most interesting is what Brazil’s Administration Council for Economic Defense (CADE) had to say about the deal and Sony. Brazilian regulators wrote in response to Sony complaints:

“Furthermore, it is important to highlight that the central objective of CADE’s activities is the protection of competition as a means of promoting the well-being of Brazilian consumers, and not the defense of the particular interests of specific competitors” Source

The comments by Brazilian regulators are another reminder that as of current, this merger would only result in closer competition between Microsoft, Sony, and Tencent in gaming. Sony feeling most threatened by the deal due to the perks of their existing deal (ends in 2024) with Activision over the Call of Duty franchise have been the most outspoken against the deal going through. Microsoft has continued to reassure regulators of their commitment to keep the CoD franchise on all platforms past the 2024 deal end & release the CoD games at the same time on all platforms. I take the comments by the Brazilian regulators as another reminder of who is atop the gaming industry and how the Microsoft-Activision deal is not what it seems like at first glance.

The Deal

(1) Deal Likelihood is calculated using the current spread on the deal ($22.40) versus the total accretion of the deal from the market clean price ($35.63). The market’s assessment of likelihood should be the ratio of what is left to be accreted over the total accretion possible, which is 63% $(22.40/35.63).

(2) Clean Price calculated using pre-deal per-share price compared to the decline of the S&P 500 since (17.75%) using the target company’s beta, 0.52 (5yr, monthly). The clean price represents what the target company would be trading at today had there not been an offer tabled.

In the image above, I’ve presented the current situation of this merger and the potential gains/losses for an arbitrageur. It is obviously difficult to know the exact likelihood of the deal passing without having any strong legal knowledge in the matter. Microsoft has a terrific record of seeing out past acquisitions which they should hope to see continue here. The downside as implied by the calculated clean price would be a drop of 22.28%, should the deal fail to close. So, although the gain is handsome, the downside is not too appealing. In my mind, I see this deal following through in the UK, EU, and US for the same reason it has in Brazil & Saudi. Microsoft’s purchase of Activision, although large would result only in the closing of the gap in revenues from the 2 frontrunners in the industry, Sony & Tencent. So, I think the market’s hesitancy over this deal presents an opportunity that doesn’t come often. Thankfully, we won’t have to wait too long to learn more about this deal as we await a preliminary decision (either further probe by 90 days or accept) by EU antitrust regulators on November 8, 2022. Other antitrust regulators are still investigating with decisions to be made in the short future (UK’s CMA phase 2 investigation deadline is on March 1, 2023).

In light of the sustained high inflation we are seeing today, I thought it would be great to read over and summarize the writing of Warren Buffett from his experience with high levels of inflation in the 70s. In 1977, Buffett wrote for Fortune magazine on “How Inflation Swindles the Equity Investor”, a time where most believed equity investing was a ‘hedge’ against inflation. No one knows how this period of inflation will unfold today but it should be interesting to learn what Buffett made of a period where inflation ruled the land.

Effects of Inflation

Buffett begins by explaining how there is no secret that stocks and bonds perform poorly in inflationary environments. With bonds, it is axiomatic that a fixed income investment will perform poorly when the dollar value in which it is denominated in continues to deteriorate. Back then, many had believed stocks to be a hedge against inflation, which proved to be misguided. The reason as Buffett puts it, at their economic substance, a stock is very similar to a bond. The main difference between bonds and stock is the unpredictability of their cash flows, a stock varies from year to year, a bond has set coupon payments.

Through the 50s, the market had an annual average year-end return on equity of 12.8%. Into the 60s &70s the average sat at around 10.8%. While the return on equity could jump around yearly, over long periods of time it was quite stable, this is where Buffett believes it would be okay to refer to corporate earnings as an “equity coupon”. A key difference between bonds and stock is when the cash ins received by the investor, usually a bond coupon is handed straight to the investor to reinvest wherever they see fit. As for stocks, earnings withheld are reinvested at whatever rates the company happens to earn. Part of this earnings can be paid out in dividends, the rest will match the company’s rate of return. This ability to reinvest earnings at high rates allowed for investors to buy interests in enterprises for a price at book value, which was far below the actual value of the business.

When inflation rises and interest rates follow, the equity return starts to be looked at differently by investors. Although, Buffett claims that over the long term, the equity coupon is more or less fixed, the short term fluctuations can sway investor attitude about the future far more than warranted. Since stocks have no maturity and carry additional risk to bonds, investors need a return above that of a bond and when this spreads narrows too much, the exit is the option for most investors.

The Inflation Tax

Further into the article, Buffett breaks down the mathematics of the inflation tax. Had an investor been earning 12% pretax they were expected to earn 7% aftertax using tax rates from that time. When inflation runs at or above that 7% rate, the real return becomes zero. Another example Buffett uses, is a widow earning 5% on her savings. Had the widow been taxed 100% on interest income she would lose her 5%, had there been no interest tax but inflation ran at 5% she would lose her interest income all the same. In both cases the widow walks out with no real income.

Conclusion

In sum, inflation works as a silent tax that swindles everyone including the equity investor. The effect on inflation can affect aftertax returns. When you boil it down, investing at its core is the commitment to give out your purchasing power today in the hopes of increasing your purchasing power later a much higher rate. Periods of sustained high inflation are not able to guarantee the return an investor receives after frictional costs will actually see them make real returns. So it should also follow, that periods of deflation are more favourable to equity investors, where the real return on their investments would increase due to future higher purchasing power of their dollar invested. Many people attempt to guess the inflation or interest numbers, and work off that, but those numbers move in a way that could never be predicted, not even by those with access to the necessary information. Inflation is a tax investors must familiarise themselves with and beat or they end up earning zero real returns if the rate of inflation is high enough.

Adobe is one of the largest software companies in the world. The company offers a line of products used by photographers, editors, designers, content creators, and students. Many of the products offered by Adobe work through a Software-as-a-Service (SaaS) model. The company organized its operations into 3 segments: (1) Digital Media (2) Digital Experience (3) Publishing & Advertising. The digital media segment’s flagship offering is the Adobe Creative Cloud subscription service. This service is most closely associated with the Adobe brand. The Creative Cloud includes Photoshop, Illustrator, Acrobat, and 20+ apps in the service. Although these services have been offered for a long period of time already, with a growing creator economy the runway still has a long way to go. The digital experience segment flagship, Adobe Experience Cloud & Adobe Analytics, is an enterprise service used to manage the customer and business experience. The experience cloud offers SaaS solutions to customers through web browsers. The last segment, publishing and advertising, is much smaller and really focuses on helping businesses in their advertising pursuits coupled with low-end desktop publishing products.

The Earning Power of Adobe

Greater than 90% of Adobe’s $15B revenue comes straight from its subscription services. These subscriptions are software based and result in incredible margins for the company. Adobe’s last fiscal year saw net earnings margin of 30%. At a time where inflation is running rampage, the lack of need to spend heavy amounts in operations will prove to be very kind to Adobe relative to other companies. One of Adobe’s key competitive advantages along with the economies of scale in being a software application provider, is its brand recognition. Anyone, creative or not, looking to edit a photo knows exactly which app to use – Photoshop. Customers in niche groups will already be well aware of which Adobe application is best for their use cases. Personally, I am no creative but I already associate Adobe with any sort of video and photo editing. There are other competitors in this field but they lack the customer captivity a brand like Adobe has spent years building. Just to show how strong Adobe’s earning power is, in the 2 year period from Nov. 29, 2019 to Dec. 3, 2021 total revenue grew 41%, this period was the 37-39th year of operations. Adobe is a fantastic company operating with exceptional economics that has been creating value for shareholders for many many years.

Adobe & Figma

Adobe has recently been in the news for its proposed $20B (cash & stock) acquisition of Figma, a collaborative web application. Adobe shares fell roughly 20% after news broke of the planned acquisition. It is clear investors are worried about the company paying such a large price for Figma. There are also concerns that regulators will step in to stop Adobe consolidating more businesses in a market it already confidently dominates. From what I’ve gathered Adobe would be acquiring a company known for its collaboration and design – beating out Adobe’s related products. This should help Adobe form a new image of themselves in this section of their business. What seems to scare investors the most is the price tag, which is 50x Figma’s current annual recurring revenue (ARR). The company has grown in leaps over the past decade and is still continuing to grow its ARR at a strikingly impressive rate. There is too little information out to decide whether the valuation Adobe is putting on Figma is far too expensive but I can see why some argue it is – as always time will tell.

Conclusion

Adobe is a great business and has been for many years. The company operates with monopoly-like economics and seems poised to do so for many years to come. The business has grown phenomenally as a result to its switch years ago into a subscription based service. The SaaS model it has implemented continues to provide high returns on equity and a very kind free cash flow yield. Adobe has proven to be a wonderful generator of shareholder wealth over the years and only time will tell if it can continue that form into the future.

Credit Acceptance (NASDAQ: CACC) is an auto finance company that provides used-car loans to primarily subprime borrowers. Credit Acceptance’s business model deviates from the industry norm of buying loans originated from a dealer at a modest discount (although CACC does practice this under their “Purchase Loan” program). Instead, Credit Acceptance’s main focus is their Portfolio Program, where they act as an indirect lender (legally) by partnering with dealers to make the loans. Credit Acceptance sends the dealer an advance for anticipated future collections of the consumer loan. The dealer also receives a down payment from the consumer on the loan. CACC then receives 100% of the cash flow from the loan up until the amount equals that of the advance sent by CACC to the dealer plus some profit (130% of the advance – profit is called the servicing fee). After receiving the full balance, CACC and the dealer split the cash flows, typically 80-20 (20% for CACC). This works for both the dealer and CACC due to the potential profit to be made from successful consumer loans.

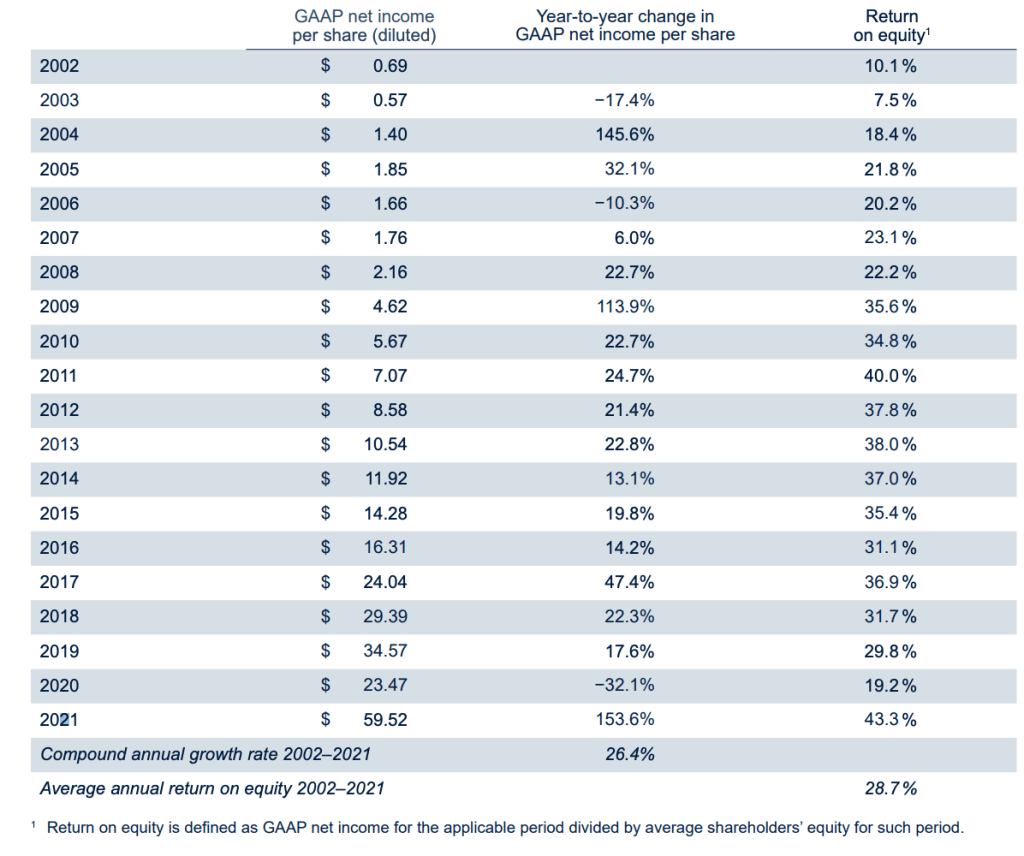

Credit Acceptance has been using this model for well over 20 years now without fail. The result from its operations have compounded diluted earnings per share at 24.9% over the past 20 years as well as an average return on equity of 28.7%.

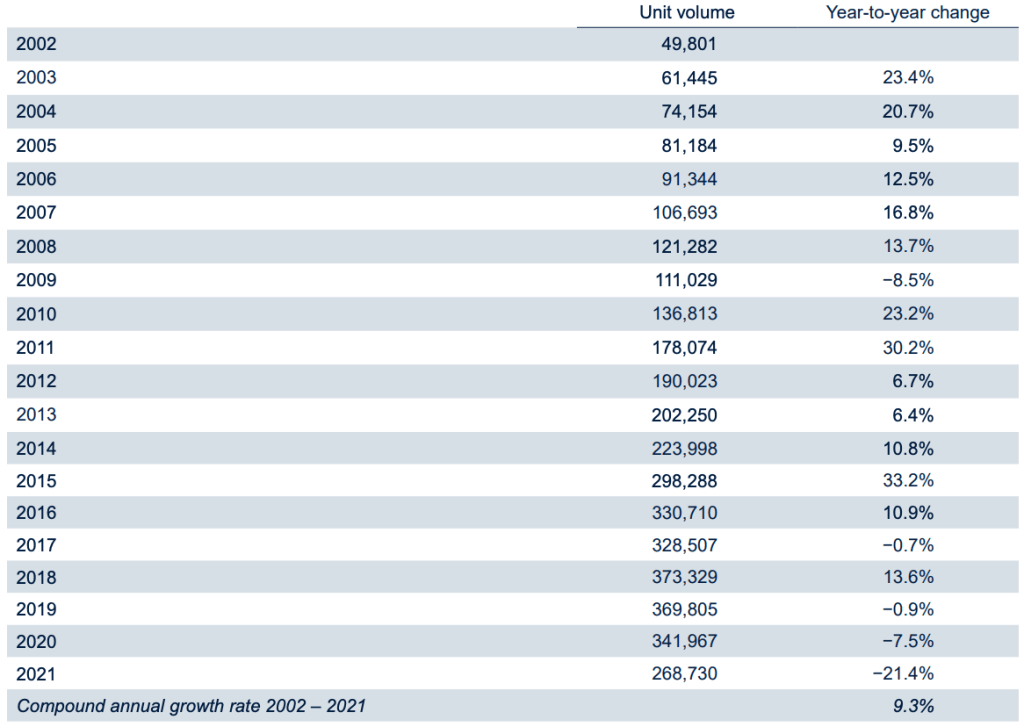

Over the past 20 years, Credit Acceptance has grown unit volume at a compounded annual rate of 9.3%. But in the past 3 years, unit volume has declined markedly. CACC already has 11,000+ dealers and with some sources estimating only 27,000 dealers in the country it will be a tough ask to expect more active dealer growth.

The past 3 years do show a potentially worrying slowdown in unit volume that could be indicative of CACC’s struggle to continuously find new dealers. Another possible explanation is the extremely loose monetary policy environment of the past couple of years. For the 3 months ended June 30, 2022, unit volume grew 5.1% vs 2021. However for the 6 months ended June 30, 2022, unit volume fell 10.5%. It is too soon to tell how the current change in interest rate policy will affect CACC but going off past cycles, there is reason to believe it will be a positive for the business. It seems that Credit Acceptance has no problem shredding some of its market share in competitive environments, knowing it will make it up when tighter monetary conditions emerge.

Business Risks

The 2 biggest risks Credit Acceptance faces are regulatory & default in my opinion. Starting with the latter, in 2021, 91% of unit consumer loans came from individuals with either no credit score or a FICO score below 650. It is difficult for many to accept a business only collecting 66.5% of their total loan value in a year.

The regulatory risk comes from moves to modify CACC by the Consumer Financial Protection Bureau (CFPR). Many individuals that defaulted on their loans have sighted CACC’s high interest rates and fees to be predatory. CACC claims that their business connects those that may never have got the chance at financing to dealers that also would’ve missed out on these consumers without them. There is some truth in this claim. However, it is very difficult to claim to be benign when you charge subprime borrowers 20-30% on loans. As the CFPR and other state attorneys clash heads with CACC, the business may incur material costs or be forced to change their business model.

Conclusion

In sum, Credit Acceptance is a company that has compounded earnings at a remarkably high rate for the past decades. The company to this day still continues to return great wealth to shareholders. For the 6 months ended June 30, 2022, CACC repurchased 8% of shares outstanding, the mark of a business with excellent economics. CACC does face the problem of having very few reinvestment opportunities as seen with the shrinking unit volume per dealer count. Credit Acceptance is a business with exceptional economics but may struggle to continue compounding at such high rates well into the future.

Alphabet Inc, the conglomerate that owns Google and its subsidiaries is one of the most fascinating companies in the world. In this post, I will focus more on the Google business of Alphabet Inc.

Google is divided into 2 main segments: Google Services & Google Cloud. Alphabet continues to innovate in the technology space, spending over $100 billion in R&D over the past 5 years, making significant commitments in AI.

Google Services

The core products/platforms in the services’ segment include: ads, Android, Chrome, Gmail, Google Drive, Google Maps, Google Photos, Google Play, Search, and YouTube.

As mobile adoption continues, people consume more videos, books, games, music, and ads. The company continues to invest in both the Android & Chrome operating systems in a bid to form a tightly knit family of hardware devices as well. Alphabet also owns the Pixel Phones, Fitbit, and Google Nest. The Services segment generates revenue mostly through advertisements (performance & brand). Performance advertising involves creation of ads that users will click on, to lead them to the advertisers. Brand advertising involves helping specific brand advertisers reach their specified audience through text, video, or image across various devices. Google Services also has other sources of non-advertisement revenues. Google Play generates revenue through app sales & in-app purchases of content from the Play Store. The hardware produced by Google (ex: Fitbit, Nest, Pixel) all generate sales from units sold. YouTube subscription services (ex: YouTube Premium, YouTube TV) also provide a source of non-advertising revenue.

Google Cloud

The core products in the cloud segment include: Google Cloud Platform & Google Workspace.

The main source of revenue from the Cloud Platform comes from infrastructure, platform, and other services. Workspace generates revenues mainly from enterprises using cloud-based collaboration tools (ex: Meet, Drive, Calendar, Docs, Gmail).

Google’s Moat

I believe Google’s greatest strength is in its customer captivity – most prevalent in the largest unit of the business, Google Search. I cannot think of a time in my recent memory where I’ve seen or used a different search engine to Google. I believe this is the same for the majority of others. The competitors in this field are shrimp compared to the whale that is Google Search, and the economics of Search shows it. In the video content space, YouTube also remains king. There is fierce competition in this arena, as you compete for consumer attention. However, YouTube unlike a Netflix or Disney+ does not need to focus on creating its own content, when YouTubers do the expensive content creation for them – a wonderful system for both parties involved. The other main competitors for attention come from social media (ex: Instagram, TikTok) have shown that in the case of long-form content they still cannot compete with YouTube. In short videos, where TikTok rules, Google & Facebook have both introduced their own competitors which are growing at healthy rates to perhaps stifle TikTok’s popularity. It is too soon to say who will end up winning the fight of the short form content platforms, but the already concluded battle of long form content platforms is being dominated by Google’s YouTube. Another unit worth mentioning is Alphabet’s Android. The mobile OS has a 47.5% market share of mobile OS as of 2018 (IOS behind with 41.9%) allowing Alphabet to recoup a large pot for themselves from the Play Store. This shared dominance with IOS is unlikely to change with new entrants in a field where consumers are hesitant to change. Alphabet’s position in the markets it finds itself allows the company to produce above average returns on capital. I mentioned that they spend heavily on R&D earlier on, it is important to remember that the nature of most of its business does not require heavy CAPEX. Alphabet’s core business allows for great economics where the shareholders can generate great wealth for themselves through ordinary business operations, a truly remarkable enterprise.

Quantitative easing (QE) is a common form of unconventional monetary policy that is frequently referred to as money printing – incorrectly. QE does not involve the creation of notes and coins by central banks, which is still only a small portion of overall money supply. If QE is not money printing, then what is its purpose and is it directly inflationary? In this post, I’ll attempt to provide an explanation of what QE is and the process of money creation.

The Myth of the Money Multiplier

It is a very wide misconception that banks simply act as an intermediary lending out deposits made by other savers. In the modern economy, this is simply not true. Lending creates deposits, not the other way around. Private banks are the creators of deposit money and have no limit on their funds available to lend as long as they meet regulatory liquidity requirements. As private institutions, banks decide how much they wish to lend based on the profitability of available lending opportunities. Importantly, there is nomoney multiplier. The demand for loans from these banks rely heavily on the prevailing interest rate on these loans. While central banks do not control the amount of reserves, they can set the ‘price’ of reserves through interest rates.

The Process of QE:

Central banks’ preferred monetary policy tool is setting the interest rate (bank rate) on bank reserves in the overnight lending market. This should then effect a number of interest rates in the economy, such as bank loans. However, there is very little proof of this tool effecting longer-term interest rates in the economy and central banks run into a problem when the interest rate (bank rate) on these reserves are already near zero, while spending in the economy is not consistent with the central bank’s objective. The most common response is quantitative easing, which is just the central bank purchasing assets (ex: long-term government debt, mortgage backed securities) from mostly the non-bank financial sector (ex: insurance companies, pension funds). Since only commercial banks have reserve accounts at central banks, they are used as an intermediary in this transaction. In effect, when a central bank wishes to buy assets from a pension fund, the pension fund’s bank would credit its account by $x. The central bank would then credit the private bank’s reserve account (w/ equivalent $ amount) to finance the purchase.

As shown by the image above, there is only a change of financial asset composition in the private sector, no new money was printed as a result of QE. The increase in commercial bank reserves at the central bank have no effect as they cannot be lended to consumers within the economy. Since QE initially increases the pension fund’s deposits, the fund is likely to deploy those deposits in higher-yield assets (ex: shares). Some argue that the asset swap performed by QE has little inflationary effect as the new deposits will only be used to buy assets in the financial sector and is not in the hands of consumers. Others argue that as a result of the central bank buying longer-term debt, the yields of these assets should fall along with longer-term interest rates. This then creates a favourable environment for lending to stimulate spending/investment within the economy

In sum, quantitative easing is not money printing, but an asset swap by the central bank to stimulate the economy. The increase of bank reserves does not directly go into the hands of the people in the economy as it is only to be used by actors with reserve accounts at the central bank. Although, central banks have enormous influence over the amount of money in the economy, there is no direct control of the monetary base. The majority of the money in circulation comes from commercial banks as opposed to printed by central banks. When the bank rate in the overnight market does hit its effective lower bound, it is appropriate for the central bank to begin an asset purchase program (QE) in the hopes of raising prices across the economy.

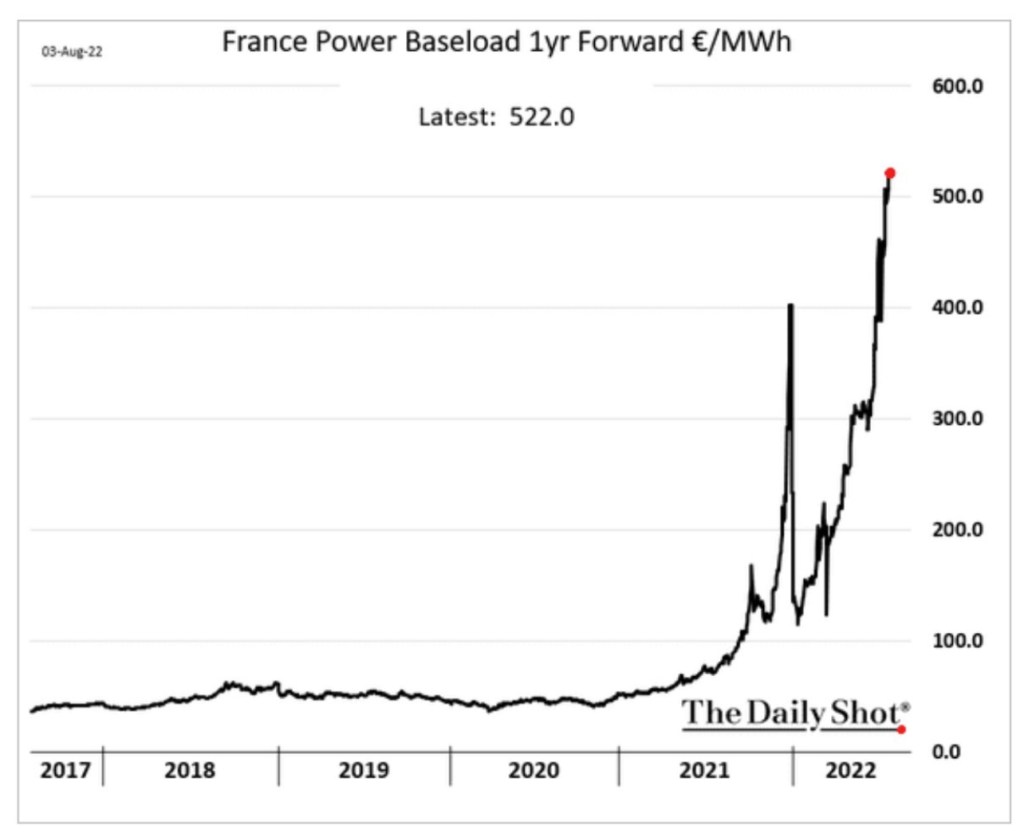

The effects of Russia’s invasion of Ukraine are contributing to an economic downturn across Europe. In response to governments across the continent sanctioning Russia, Moscow has retaliated by cutting natural gas deliveries into the European Union. For many years, Western European nations assumed that regardless of geopolitical issues Russia would be a dependable source of energy. Throughout 2022 it has proven not to be the case.

As the end of summer nears, European energy security is clouded with uncertainty for the winter to come. Worries picked up after Gazprom cut Nord Stream pipeline gas flows from 40% to 20% in the backend of July, sighting problems with turbines. The Nord Stream pipeline is the main point of entry of Russian gas into Europe and at full capacity could supply enough gas to satisfy 10% of the European Union’s annual consumption. Without Russian gas, European industries will be hit hard and may end up rationing gas in the winter.

The German government has taken a 30% stake as part of a larger $15.3 billion (15 billion euros) bailout of energy giant, Uniper. Uniper had found itself bleeding cash as it was forced to buy supplies from the highly-priced gas spot market after not receiving the contracted gas volumes from Gazprom. The bailout also includes an increase in the credit facility for Uniper to 9 billion euros (previously 2 billion) at state-owned KfW bank. Uniper shareholders would also be involved in the bailout as the plan would see their ownership interests diluted, a ban on dividends, and a cap on executive compensation. Finnish majority-owner Fortum had an 80% stake before the bailout, it now only holds 56%.

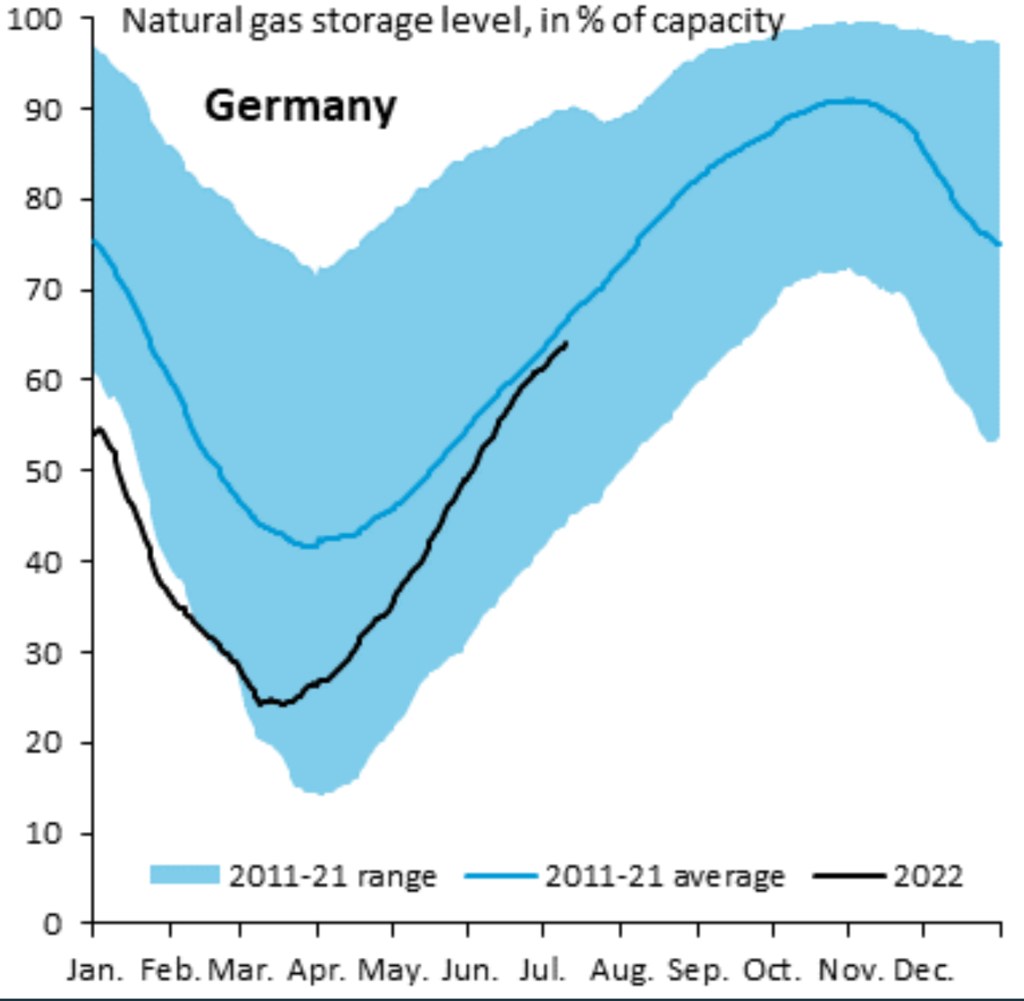

Germany usually likes to keep its gas storage level at around the 90% mark by late fall, going by the past decade. With Nord Stream running at 100%, this level would comfortably get Germany through the winter. However, Nord Stream is only running at 20% right now, meaning it is almost impossible for storage levels to even hit the 90% level in time for the winter. Without Russian cooperation to drastically increase gas supply it is looking very likely that Germany will have to ration its gas for the winter months.

Photo: Twitter, @RobinBrooksIIF

In France, the government offered to nationalize the EDF, the largest owner of nuclear power plants in the world. The Finance Ministry tabled an offer at €12/share (a 53% premium to market price at the time). The French government’s decision comes at a time where the EDF is operating at a loss as a result of government caps on electricity prices. Additionally, the EDF also had to shut down 12 of its nuclear reactors (total of 56) for maintenance due to unanticipated corrosion.

As a result of Russia’s unreliability, European countries are looking for alternatives in North Africa and the Middle East. Agreements between the producers and Europe are filled with complications. Qatar looks like the best bet for the European countries but negotiating the concessions of such an agreement will require significant time. The European Union had launched an antitrust investigation into Qatar’s restrictions on reselling gas as it limits cross-border trade – the probe has since been dropped. Other points of contest have been over the length of contracts and the pricing due to Qatar’s distance from Europe. Other nations in Northern Africa (ex: Algeria, Libya) are by most not considered viable due to the accompanied political risk.

Politicians in Europe have began calling to lift the Russian sanctions, hoping to ease the energy crisis their people face. As usual, this is an issue most political parties are unable to agree on.

Pakistan, like most of the economies in this post struggles with inflationary pressures and is faced with high default risk. The inflation rate hit 21% earlier this year. To combat this high inflation the central bank has raised rates to 15%. The government has also cut back on fuel subsidies and raised taxes. Government action was largely pressured by the IMF for exchange of a $4 billion bailout package (receiving $1.2 billion upfront). The people of Pakistan have voiced their frustration of government austerity-like measures as well as the rising cost of living. The country had been victim to dwindling foreign exchange reserves (approx. 2 months’ worth of exports) and requested for an IMF bailout, which they have since received. China has also stepped up and reduced the rate of their $2 billion loan. Only time will be able to tell whether Pakistan can escape their financial troubles without default.

Ghana

A similar story holds in Ghana like many emerging markets are also running alarmingly close to defaulting on foreign debt. The country’s government debt is a staggering 82% of total GDP. The Ghanaian cedi is already down 24% YTD against the dollar. The country also is fighting a 20-year record 29.8% YOY inflation rate. The lack of government funding has led to some schools across the country not providing any lunch food or school supplies and are being put at risk of indefinite closure. The government has already began seeking out a $1.5 billion bailout from the IMF to avoid “full blown crisis”. The cost of living has already sparked protests within the country in which police had to be deployed with rubber bullets and tear gas. The largest teachers’ union has also demanded a cost-of-living adjustment to deal with the inflation or else they would go on strike. Ghana’s situation is yet another example of the struggles of emerging market economies currently.

Egypt & Rest of the World

Many more emerging economies are also victim to the effects of inflation, a retreat in foreign investment due to increased interest rates and/or other factors in investment decisions. Countries like Egypt and Tunisia are seeing rises in food prices and trouble meeting foreign dollar debt obligations. Due to political risks surrounding the change in Tunisia’s constitution (US heavily against) the IMF looks currently unlikely to bail the nation. It seems the IMF would consider loaning to the Egyptians however. The inflation problem continues to many other nations in the region. Sudan saw its annual inflation rate hit 192% as well as civilians protesting the new military leadership. In Lebanon food prices have tripled and civilians go many hours in the day without electricity. Many Ugandan citizens have looked to flee the country in search of work in the Gulf states. All these problems have lead US General. Townsend to warn Washington of potential unrest and coups in the region.

Outage in Beirut, LebanonSudanese Protests

Rising prices for Egyptian staple (baladi bread)Protests in Tunisia over proposed constitution change

Laos

In Laos it is still very much the same story as other emerging markets. Low foreign exchange reserves, hefty debt repayments coming due, and a sinking currency all in one. The country recently had its credit rating cut by Moody’s to reflect the risk of holding Laos debt. Over 50% of Laos debt is controlled by China so their troubles could be eased if the Chinese renegotiate the terms of the debt in question. Leadership in the country has already cut back on spending, implemented strict capital controls, and using their authoritative power controlled the narrative to the masses.

As the global interest rate environment changes instances of unrest in countries around the globe will continue to emerge.