History

TSMC was founded by Morris Chang in 1987 through funding from the Taiwanese government, wealthy Taiwanese businessmen, and Phillips (retaining a 27.5% stake in exchange for production technology and IP licensing). Before its founding, Chang was previously an executive at Texas Instruments and had conjured the idea of a ‘pure play’ foundry. He had pitched the idea to other executives at TI and later Moore and Grove at Intel but ended up being rejected all the same. At the time there were no ‘fabless’ design companies, so it was seen as a gamble into a market that didn’t exist. It is now clear that Chang’s prescience has put TSMC at the forefront of semiconductor manufacturing.

Overview

TSMC’s market cap today is US$500 billion. The company has a 60% market share in the foundry business and an analyst estimated 90% market share in advanced logic manufacturing. TSMC is without a doubt one of the few companies with a durable competitive advantage evidenced by the stability of its market share over the years.

Fab Economics

TSMC categorizes their fabs into three types: mini, mega, and giga. Mini-fabs produce 10-25k wafers a month. Mega fabs produce 25k-100k wafers per month. Giga fabs produce greater than 100k wafers per month. Fabs are near identical regardless of classification; with giga-fabs simply being a scaled-up version of their counterparts.

The costs of building a fab have continued to rise through the years. In 2010 it cost TSMC ~$9.5 billion to build a 12-inch giga-fab in Taichung (Fab 15). Just 8 years later, Fab 18 (another 12-inch giga-fab based in Taiwan) would cost them ~$20 billion. Much of the increase in costs can be explained by elevated pricing of the machinery fabs house (e.g., photolithography machines). It is estimated that ASML’s new high-NA EUV technology will cost anywhere between $300-$400 million per system, a fee that limits potential customers to the very few with deep pockets.

Note: TSMC estimated in 2020 that they had 50% of all active EUV tools installed – putting them well ahead of their competitors. Some commentators estimate that in 2023 TSMC has 3x as many machines as Samsung (39) and 6x that of Intel (20).

Manufacturing semiconductors requires a focus on quality (yield), speed (cycle times), and volume (wafer shipments). TSMC has been able to optimize for all three. Cycle time refers to the number of days it takes to go through a mask layer (DPML) – where lower is better. In the 90s, a 180nm chip had about 25 layers and took 2 days to get through a layer. Appropriately, the full 25 layers would take 2 months. As processes improved so did the number of layers in a wafer. It is estimated that a 5nm chip would be 115 layers if not for EUV technology limiting it to the 81 layers it has today. If TSMC hadn’t improved cycle times it would take ~8 months to get through a wafer. The end-customers TSMC provides simply do not have the ability to wait long enough that long as technology constantly evolves. Delays are costly for manufacturers and their reputations.

Yields refer to the % of chips produced from a wafer versus the total number that could’ve been produced. Wafer shipments refer to the number of 12-inch wafer equivalents the company produces. There is a feedback loop between all 3 elements; as a foundry produces more chips (higher volume), they learn how to improve the process (better yields & speed) and can take on more and new business from customers (higher volumes).

Customers & Competition

TSMC has meaningful customer revenue concentration. Their top ten customers accounted for ~70% of their revenues in 2022, with their largest customer (Apple) accounting for 23%. I believe that the concentration of revenue within the top customers is not a business risk as conventionally thought of.

TSMC’s customer base gives the business an advantage against its competition. TSMC attracts the highest calibre customers in the chip design business (i.e., Apple, AMD, Nvidia, etc…). These companies order chips at high volumes and have the coffers deep enough to pay TSMC premium prices for said chips. The large swaths of volume ordered by top customers enable the TSMC machine to ramp-up production, learn from the ramp-up, and importantly, improve the yield on manufactured chips.

Differentiation

The linchpin of the TSMC foundry model is Chang’s promise (that has since been kept) that the business would not enter the chip design business. This promise has helped differentiate TSMC from its close competitor, Samsung. As TSMC refuses to design chips, companies such as Apple who directly compete with Samsung would rather send their designs over to TSMC.

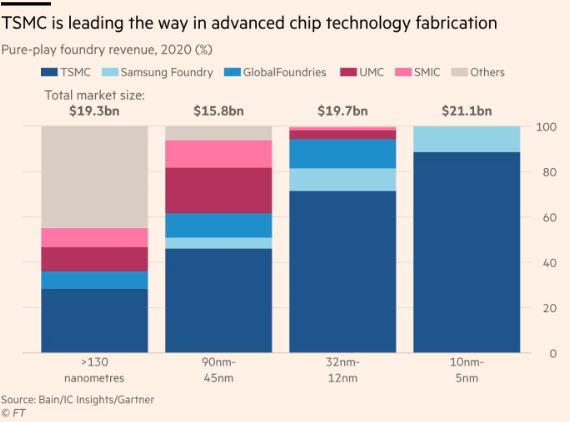

Alas, TSMC is still forced into sharing the stage with other foundries (i.e. Samsung). Chip designers would understandably prefer to not be held hostage to one manufacturer. This has led several customers to bifurcate their designs to Samsung and TSMC – the only two players at the leading edge (7nm processes and below) as of current. For non-leading edge processes, the market is more fragmented with other players (e.g., GlobalFoundries, SMIC, UMC, etc…) able to compete as the costs of entry are much lower than the advanced processes and research is far less intricate.

Moore’s Law

Before moving onto my investment thesis, I think it is most important to consider the history and possible death of Moore’s Law. Moore’s Law dictates that the number of transistors on an integrated circuit would double every two years and the cost of computing (to the consumer) would fall appropriately.

Today, there are several industry figures proclaiming the death of Moore’s Law. The most notable being Jensen Huang, the cofounder and CEO of Nvidia (although other industry leaders disagree, see Pat Gelsinger at Intel). The idea being that transistors cannot continue being shrunk and eventually the laws of physics will put an end to the shrinking. Additionally, it may end up being too costly to manufacture them before reaching such a point.

This is not the first time in history that Moore’s Law has been decreed as dead. In 1988 an expert at IBM, Erich Bloch, concluded that Moore’s Law would stop working once a transistor shrank to 1 micron (1000nm). Transistors would go onto be shrunk past that size a decade later. I think the correct answer to whether Moore’s Law is dead is a simple ‘who knows’. Irrespective of whether transistor density can continue to grow at some historical pace, TSMC is well positioned to extract value from the industry.

Thesis

Morris Chang credits Pat Haggerty for using the word pervasiveness to describe the semiconductor industry. If semiconductors are pervasive, no one company will be able to design all the products that use them. Washing machines will use them, automobiles, data centers, PCs, smartphones, and the technologies of the future all will too. The idea that enabled the success of the foundry business model still exists today. In an industry where the suppliers are concentrated and the buyers plentiful, it will be the suppliers that hold the key. In the semiconductor industry the keys are firmly placed in the pockets of the foundries, and at the leading edge – TSMC.

Financials

TSMC sells their chips to 5 different end customers, with the High Performance Computing (HPC) and Smartphone platforms accounting for ~80% of total revenues. Other platforms include automotive, digital consumer electronics, and the internet of things. HPC and smartphone platforms tend to require leading edge chips, which make up ~60% of TSMC’s revenues.

Over the past decade, TSMC has been able to grow FCF at a 25%+ CAGR and deliver a return on invested capital of ~20% in the same period. Although the business requires lots of capital expenditures, the return TSMC earns on those investments is remarkably high. If the reinvestment opportunities continue to present themselves at similar rates, it is a no-brainer for the company to continue making such value accretive investments.

Valuation

TSMC is expected to earn revenues of US$69 billion come the end of fiscal 2023 with operating margins of ~50%, with its largest expense being R&D – accounting for ~7% of total revenues. Although the semiconductor industry is known to be fraught with cyclicality, over the long-term, the logic business (leading edge logic at that) is largely secular with comfortable growth. TSMC’s current EV/EBIT multiple is 13x.

However, I believe that multiples is not truly reflective of the underlying earnings power of the business. I suspect the business has underearned in the three-quarters of the trailing twelve months, resetting from the pandemic boom. In a more normalized environment I fail to see why EBIT cannot be normalized at FY2022 #s implying a normalized EV/EBIT of 11x.

I expect that TSMC will be able to grow its revenues at 10%+ per annum for the next half-decade and keep operating margins at 45% or higher. Add in the AI tailwind and I think there’s lot of potential in growth the market is not currently pricing in. Should the business be valued at its current multiple or revert higher to historic levels (~15x EV/EBIT) in 5 years I would expect a minimum 10% CAGR at current prices of $95 per-share.

Risks

The biggest risk TSMC is exposed to is geopolitics. The CCP continues to state the reunification of Taiwan and the mainland as one of its goals. The majority of TSMC’s fabs are located on the island – any disruption to operations from a conflict will be a negative for the company. In my view, the recent US push of onshoring and protectionism will only increase this risk. The less dependent China is on TSMC and the reminder of the chip industry, the less care would be taken of TSMC’s fabs should a conflict arise.

As TSMC looks to diversify its fab locations away from Taiwan, the company will lose some of the competitive advantages it has. Just recently TSMC had to push the expected production timeline of its in-construction Arizona fab to 2025 due to a shortage of workers. Construction costs in the US are also ~5x that of Taiwan. The further the distance between fabs, the more friction there is, should problems arise (TSMC employees would have to fly across the Pacific rather than a trip to Japan, Korea, or a drive to the next fab). In Taiwan, the company could reliably recruit from the top universities and had a reliable supply chain at far less the cost. International diversification and labor standards will surely eat away at these advantages.

Lastly, in such a fast-paced industry, innovation from competitors will remain a risk TSMC is exposed to. Should TSMC be unable to produce leading edge chips reliably and allow their current and future competitors (Samsung & Intel) to get the jump on them they will lose customers and their edge.

Mitigations

In the case of Chinese expansion, there is no mitigation. That decision is left to the CCP Politburo, specifically, Xi Jinping. The only way to get comfortable with that risk in my opinion is through position sizing. For some that may be 0% of a portfolio for others it could be 90%, although the former makes more sense.

I do not think it is likely that TSMC loses their innovative edge. As the leading edge continues to battle the laws of physics, new entrants (Intel) will have a long way to go before they can match TSMC in terms of innovation and manufacturing process power. TSMC is constantly learning with each new iteration of its advanced processes, newer entrants will have to learn how to produce and convince customers to leave trusted partners. As Jensen Huang put it “TSMC has learned to dance with 400 partners, Intel has always danced alone.”

I am a firm believer that the best businesses are those that are doing the same thing that was done years earlier. In TSMC’s case the business has not changed since it invented the idea of dedicated foundries in 1987. I do not believe it will change its model in the next decade either barring foreign intervention.

Disclaimer: I own shares of the company discussed above.

[…] Managerial Case Study – Tom Murphy Understanding Multiples Operating Leverage & Margins TSMC Pitch Railroad Industry Primer Emirates Driving Company Pitch Discounting & M.O.S Google Pitch Share […]

LikeLike